Newline's Embedded Deposit Account Solutions (EDAS)

Overview

Welcome to the user guide for integrating the Embedded Deposit Account Solution (EDAS) with Newline! This guide is designed to help you understand and implement EDAS, enabling you to offer seamless fund storage and money movement solutions to your end users.

What is EDAS?

Embedded Deposit Account Solution (EDAS) is a bank-owned custodial deposit account product designed to enable enterprise fintechs, and SaaS platforms to seamlessly integrate compliant and scalable deposit account functionality into their applications.

Use Cases:

Payment Processing for Fintech End Users: A fintech’s core business is movement and acceptance of payments to end users. In order to easily track payments for their end users, they want to process payments through a bank custodial account and trace those payments with a unique identifier for each end user.

Embedded Business Customer Demand Deposit Accounts: A fintech platform solves an important problem for their clients, and a key component of their solution is to collect and administer client funds. In order to increase the stickiness of their platform, the fintech wants to be able to collect payments from external bank accounts and store those funds in business demand deposit accounts that are embedded into the fintech’s platform.

Product Features

-

Account Type: EDAS supports two types of deposit accounts, each designed for different use cases and levels of control:

-

Custodial Accounts: Pooled deposit accounts held by the bank to manage funds on behalf of your end users. These accounts allow platforms to track user-level balances without issuing individual bank accounts.

-

Business DDAs: Traditional demand deposit accounts issued directly to the platform or business entity, used for managing operational funds or specific business workflows.

-

Bring your own Ledgering: Clients maintain their own sub-ledger system to track balances and transactions.

-

Integrated Payment Services: Supports ACH, Wire, Real Time Payment (RTP), Book Transfers, and Checks.

-

Virtual Reference Numbers (VRNs): Unique identifiers used to tag and route externally originated payments to the correct end-user sub-ledger

-

Newline APIs: Used to process outgoing & incoming payments originated from a client’s platform. When subscribing to VRNs, a client will use the Newline API to track payments originated outside of the client’s platform.

How does EDAS work?

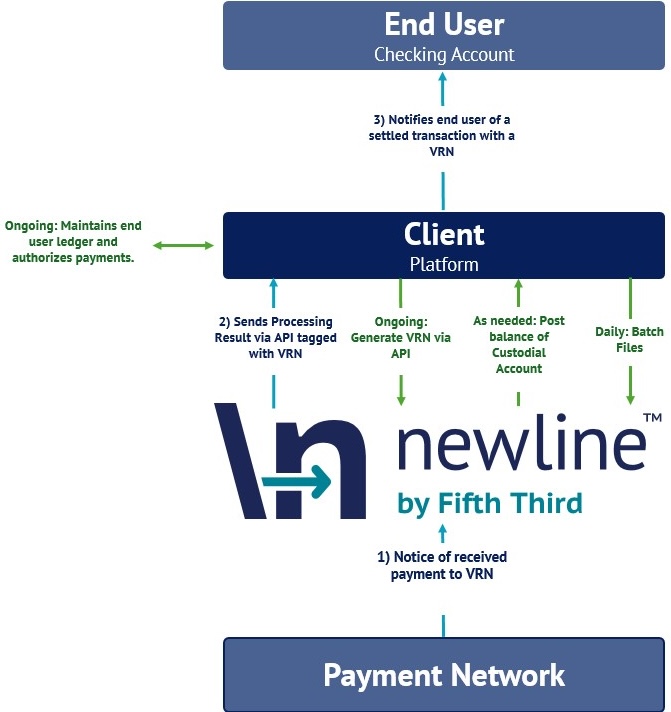

EDAS enables platforms to offer bank-issued DDAs. Funds are held in Custodial Accounts, allowing platforms to manage user-level balances while Newline oversees compliance and monitors transactions. Payments can be received and sent via ACH, Wire, RTP, and book transfers, with flexible identification using Virtual Reference Numbers (VRNs).

Payment Originated from Client Platform

The client platform initiates a batch payment. Funds are disbursed from a custodial or business DDA account, with user-level balances tracked via the platform’s sub-ledger.

Payment Originated from External Bank Account

An external bank sends a payment to the platform. The transaction is tagged with a Virtual Reference Number (VRN) to ensure accurate routing to the correct end-user sub-ledger.

Updated 11 months ago

What’s Next

To ensure a seamless integration with Newline, please refer to the following essential documents. These resources provide detailed instructions and specifications necessary for connecting to Newline's systems and managing your account operations effectively.